Vietnam: Engineered Growth and Its Limits¶

The Story¶

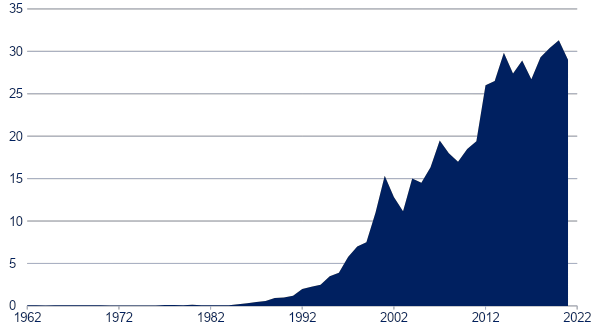

Vietnam barely grew coffee before the 1990s. What happened next was not an accident of geography or comparative advantage. It was a policy project. Through deliberate government intervention, the country went from near-zero to the world's second-largest coffee producer in about 15 years. Today approximately 600,000 farmers supply roughly 20% of global coffee volume, almost entirely Robusta.

The growth was engineered. The government treated coffee as a strategic export crop and built the conditions for expansion from the ground up. Land reform gave farmers secure ownership of their plots, a precondition for any long-term investment in perennial crops. Credit programs put capital in farmers' hands. Extension services transferred agronomic knowledge. And crucially, the government chose not to control the marketing chain: private collectors, traders, and exporters competed freely for farmers' coffee.

Farmers responded rationally. With secure tenure, access to credit, and functioning input markets, they invested in their land. The result was explosive expansion across the Central Highlands, primarily Dak Lak, Lam Dong, and Gia Lai provinces, driven by thousands of individual household decisions, each responding to the same clear incentives.

The sector's growth metrics are extraordinary by any standard. Vietnam achieved the highest farm-level yields in the global coffee industry, over three metric tons of green coffee per hectare. Farmers earn approximately 95% of the export price (per the TechnoServe / IDH 2013 Vietnam Country Report), the highest farmer share among major origins. The supply chain between farmer and export ship is as lean and competitive as any agricultural market you will find.

Most Vietnamese coffee farms are around one hectare. By global standards, every one of these farmers is "small." But they operate like commercial enterprises, not subsistence farmers. They purchase inputs (fertilizer, irrigation equipment), hire labor during harvest, and sell into deep competitive markets where price discovery happens continuously. The smallholder label understates the sophistication of the operation.

But the growth came with costs that conventional metrics do not fully capture.

Robusta requires irrigation. Intensive Robusta production in the Central Highlands consumes an estimated 2,822 tons of water per household per year. To calibrate that figure: total urban household water use in Vietnam runs around 137 tons per year; rural and agricultural households use about 144 tons. Coffee irrigation is not a rounding error. It is the dominant water use in the entire region, by a wide margin.

The expansion phase also involved substantial deforestation, as highland forest was cleared for new coffee plots. That environmental legacy is baked into the landscape in ways that cannot easily be reversed.

And monoculture dependency on a single crop, one that trades at a discount to Arabica and faces growing climate pressure in the Central Highlands, creates structural fragility that yield statistics obscure. When Robusta prices collapsed in the early 2000s, Vietnamese farmers had little to fall back on.

The central tension in the Vietnam case is this: by almost every conventional measure of value chain performance, Vietnam's coffee sector is a success story. High productivity. Efficient market structure. Strong farmer returns relative to export value. Rapid integration into global markets. The policy levers that drove this success (land tenure, competitive markets, enabling infrastructure) are genuinely replicable and instructive for other origins.

And yet. The environmental footprint is enormous. The water drawdown is unsustainable in a region facing climate stress. The monoculture concentration amplifies price and climate shocks. Sustainability considerations that conventional VCA does not easily quantify sit alongside the clean price-share metrics.

Vietnam forces a question that every value chain analysis eventually has to answer: what counts as success, over what time horizon, and for whom?

Map¶

The Vietnamese coffee value chain is remarkably short and, structurally, highly competitive. There are few actors between farmer and export, and no dominant institutional layer extracting rent.

Actors and their roles:

~600,000 smallholder farmers (~1 hectare each). Grow, harvest, and typically perform initial processing (drying the cherry) before selling. Unlike wet-processed Arabica origins, most Robusta in Vietnam moves as natural/dry-processed coffee, which means farmers retain more of the processing step and receive value accordingly.

Collectors and local traders, a highly competitive middleman economy. Thousands of mobile collectors traverse rural areas, buying cherry or dried cherry directly from farmers. This is not a thin market with one or two buyers per village. Collectors compete aggressively for volume, which has a direct and profound effect on farmer pricing. Competition among buyers means margins get competed away, and the surplus flows to farmers.

Exporters consolidate volumes, process coffee to export standard (green bean specification), and arrange shipping. Exporter margins are very slim; the economics of the downstream chain do not leave much to capture. Vietnam exports enormous volumes of undifferentiated commodity Robusta, which disciplines margins further.

International traders and importers purchase FOB Vietnam and distribute to roasters globally. Robusta is a commodity market; buyers are price-sensitive and sourcing decisions are made on cost.

The chain, simplified: Farmer → Collector → Exporter → International Trader

There is no dominant cooperative sector. No government marketing board intermediating between farmers and the market, extracting fees or adding processing costs. The government's role is enabling (policy, infrastructure, research, credit facilitation) rather than intermediating. This is a structural choice, and it matters enormously for the farmer share calculation.

This stands in sharp contrast to other major origins. Colombia has the Federacion Nacional de Cafeteros (FNC), a powerful cooperative-like institution that sets minimum prices, runs export operations, and manages the Juan Valdez brand, adding institutional overhead but also providing services. Ethiopia has the Ethiopia Commodity Exchange (ECX), which adds a transaction layer between farmers and exporters. Rwanda relies heavily on washing stations, which add processing infrastructure costs between farm and export. Vietnam has none of these layers. The chain is lean because the policy choice was to let it be lean.

Source: "An analysis of the role of middlemen in coffee supply chains: Vietnam Country Report," prepared by TechnoServe / IDH, 2013.

Breakdown¶

Vietnamese farmers earn approximately 95% of the export price, one of the highest farmer shares anywhere in the global coffee sector.

At March 2025 prices:

| Actor | Price/kg (green equivalent) | Share |

|---|---|---|

| Farmer | ~$4.70 | ~95% |

| Collector margin | <$0.05 | <1% |

| Exporter margin | <$0.20 | <4% |

| Export price (FOB) | ~$4.95 | 100% |

Why is the farmer share so high? Three reinforcing structural factors:

1. Intense competition among collectors. With thousands of middlemen competing for the same coffee across the Central Highlands, individual collectors cannot unilaterally hold down farmgate prices. A collector who tries to pay farmers less loses volume to a competitor willing to pay more. This competitive pressure is the primary mechanism driving surplus to farmers. It is not the result of farmer organizing, fair trade premiums, or government price floors. It is market structure.

2. No institutional intermediary. Unlike Rwanda, where washing stations add cost (and value through quality upgrading), or Ethiopia, where the ECX adds a transaction layer between producers and exporters, Vietnam's chain has minimal institutional overhead. There is no body taking a cut for coordination, certification, or quality management.

3. Simple processing. Robusta is predominantly processed as natural/dry; farmers dry the cherry themselves. This means less capital-intensive infrastructure between farm and export. No washing station to build and amortize means no washing station to pay for.

Contrast this with Rwanda, where farmers earn about 54% of the export price. The remaining ~46% in Rwanda is not simply margin captured by exploitative middlemen — much of it pays for washing station infrastructure, quality programs, and institutional support that Rwanda has deliberately built. The higher farmer share in Vietnam reflects a different supply chain design choice, not a moral achievement. It also reflects a commodity market rather than a specialty market, where there is simply less margin in the chain to distribute.

This is a useful analytical point. A high farmer share is not always the right goal. In Rwanda, the washing station infrastructure, even though it "costs" farmers a share of price, enables the quality that commands premium Arabica prices in the first place. Vietnam's 95% farmer share is partly a function of selling an undifferentiated commodity where there is little to share.

Benchmark¶

Yields. Vietnam has the highest coffee farm yields in the world.

| Origin | Yield (MT green/ha) |

|---|---|

| Vietnam | 3.0+ |

| Brazil (Robusta/Conillon) | 1.5–2.0 |

| Costa Rica | ~1.5 |

| Colombia | ~1.0 |

| Honduras | ~0.8 |

| Rwanda | ~0.6 |

| Ethiopia | <0.5 |

The yield gap between Vietnam and other origins is not marginal. It is structural. Vietnam's yields are driven by intensive fertilizer application, heavy irrigation, high planting density, productive Robusta varieties suited to the Central Highlands, and favorable growing conditions. These are not easily replicated; they require capital, water access, and agronomic knowledge at scale. But they also extract a corresponding environmental cost.

Income per hectare. The yield advantage reframes the price disadvantage. Robusta trades at a significant discount to Arabica. But because yields are so high, income per hectare in Vietnam is competitive with, and often exceeds, Arabica origins.

A Vietnamese farmer producing 3 MT/ha at $4.95/kg earns roughly $14,850/ha in gross revenue. A Colombian farmer producing 1 MT/ha at a higher specialty Arabica price of, say, $6.00/kg earns $6,000/ha. The productivity advantage more than compensates for the price differential.

This is not a universal argument for Robusta. It is specific to Vietnam's context: available water, appropriate climate, and accumulated agronomic capacity. Origins without those inputs cannot simply switch to intensive Robusta production and expect the same result.

Market position. Vietnam supplies approximately 20% of global coffee volume. It is the dominant global Robusta supplier and effectively a price-setter in the Robusta market. When Vietnamese production is large, global Robusta prices fall; when it is disrupted, prices rise. This is a different kind of market power than a specialty origin commands: volume-based rather than quality-based.

Environmental footprint. The yields come at an environmental cost that has no clean parallel in the benchmark table.

Total water demand for coffee irrigation in Vietnam's Central Highlands is estimated at 2,822 tons per household per year. For context: total urban household water use is about 137 tons per year. Coffee irrigation is more than 20 times the baseline household water requirement. The region's groundwater table is declining. Climate models project increasing drought frequency in the Central Highlands. The water math is, on a long time horizon, a problem.

No other major origin runs an irrigation program of this intensity. The high yields are, in part, purchased with water.

Recommendations¶

The standard VCA recommendation toolkit (transfer more value to farmers, reduce intermediary extraction, invest in certification and premiums) largely does not apply in Vietnam. The chain is already efficient on the pricing dimension. The levers for improvement are elsewhere.

| Recommendation | Impact | Feasibility | Position |

|---|---|---|---|

| Reduce water footprint (irrigation efficiency, shade-grown programs) | High | Medium | Priority — but requires changing practices that have been highly profitable |

| Export roasted coffee direct to consumers | High | Low | Attractive value capture but faces massive market access and brand barriers |

| Boost local coffee consumption | Medium | High | Vietnam's domestic coffee culture is growing; relatively tractable |

| Transfer higher share to farmer | Low | N/A | Already at ~95%; essentially no margin left to redistribute |

The last row is the most important benchmark in the table. In most country cases, "increase farmer share of value" appears as a top recommendation. In Vietnam, it is irrelevant. The chain has already competed margins down to near zero. This should not be taken as evidence that the work is done — the remaining work is on different dimensions.

Water sustainability is the highest-priority structural issue. Vietnam's yield advantage is partly built on irrigation intensity that is not environmentally sustainable in a warming, drying Central Highlands. Drip irrigation adoption, shade-grown programs that reduce water demand, and groundwater recharge investments are all technically available. The barrier is economic: current practices are profitable, and farmers have little individual incentive to reduce water use when the resource is shared. This is a classic commons problem, and it will require policy intervention — not just market signals — to address.

Roasted coffee export is the value addition opportunity most frequently cited in Vietnam policy discussions. Currently, Vietnam exports almost entirely as green bean commodity; the roasting margin accrues elsewhere. Building a Vietnamese consumer brand with global reach is plausible in theory but extremely difficult in practice — market access, cold-chain logistics, consumer trust in origin branding, and competition from established global roasters are all substantial barriers. The recommendation belongs in the "monitor and invest selectively" category, not "priority action."

Domestic consumption is the quietly tractable opportunity. Vietnam has a vibrant coffee culture. The ca phe sua da (iced milk coffee) tradition is genuinely distinctive and growing. Domestic consumption growth supports local roasters, adds value before export, and reduces exposure to global commodity price volatility. The market is developing without much intervention; modest policy support (reducing taxes on domestic roasting equipment, promoting Vietnamese coffee identity in tourism) could accelerate it.

The overall picture: Vietnam's value chain is close to optimized on the metrics that conventional VCA prioritizes. The next phase of development is not about who captures what share of a fixed pie. It is about whether the production system is sustainable enough to keep baking the pie at all.

Discussion Questions¶

-

Which aspects of Vietnam's coffee value chain could be considered "best in class"? Which aspects should other countries try to replicate, and which are unique to Vietnam's context?

-

Vietnam's farmers earn 95% of the export price — the highest share among major origins. What structural and policy factors enable this, and could they be replicated in a country like Rwanda or Ethiopia?

-

The environmental footprint of Vietnamese coffee production is substantial. Is this an externality that the value chain should internalize? If so, who should bear the cost — farmers, exporters, roasters, or consumers? What mechanisms could be used?

-

Vietnam's success was built on Robusta, which trades at a lower price than Arabica. Is there a case for Vietnam to shift toward higher-value Arabica production, or does the yield advantage of Robusta make it the rational choice?

-

What would happen to Vietnamese coffee farmers if global Robusta prices dropped by 30% for two consecutive years? How does their cost structure and lack of diversification affect their resilience compared to farmers in more diversified origins?

This case study is part of a series for the Value Chain Analysis course. See also: Rwanda, Colombia (archival), Ethiopia (archival).

Data last verified: March 2026